UK fintech regulation is becoming a pressing topic as industry leaders voice their concerns over the nation’s status as an emerging fintech hub. With the rise of cryptocurrency challenges in the UK and an increasingly stringent regulatory landscape, innovators are questioning the support available for startups. Many argue that the current rules stifle fintech innovation, pushing entrepreneurs to seek greener pastures abroad. The urgent need for reform in UK funding for startups is critical to ensure that the country remains competitive in the global market. As regulations evolve, it is essential for the UK to strike a balance between safety and enabling technological advancement.

The regulatory framework overseeing financial technology in the United Kingdom is under scrutiny, as many professionals within the sector highlight the obstacles facing new and existing digital finance enterprises. As a key player in the global fintech ecosystem, the UK must navigate emerging challenges that could hinder development in areas like cryptocurrency and digital banking. Amidst concerns over regulatory effectiveness and funding accessibility, there is significant pressure to revise these guidelines to adapt to the fast-paced nature of the industry. Stakeholders are advocating for measures that support innovation while maintaining financial integrity, to ensure the UK retains its influential role in this dynamic arena. Addressing these critical factors will be instrumental in fostering a vibrant landscape for future fintech endeavors.

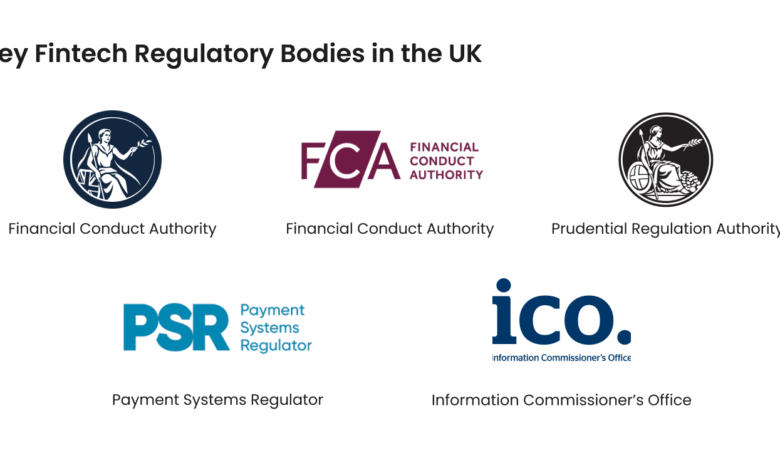

The UK’s Regulatory Landscape: A Barrier to Fintech Innovation

The regulatory landscape in the UK has emerged as a substantial barrier to fintech innovation, according to industry leaders. With the Financial Conduct Authority (FCA) enforcing stringent regulations, many startups find it difficult to navigate the complex labyrinth of requirements to establish their businesses. This overly cautious approach may stem from a desire to protect consumers and ensure financial stability, yet it results in stifling competition and discouraging bold entrepreneurs who could contribute significantly to the UK’s fintech scene.

Critics argue that such a restrictive regulatory framework contrasts sharply with the more proactive stances adopted by competing financial hubs like Singapore and the United States. As many UK-based companies face lengthy wait times for regulatory approval, potential innovators are considering relocating to more friendly environments, where there is less red tape and greater freedom to explore and unleash new financial technologies. The UK must reconsider its regulatory approach or risk becoming obsolete in the rapidly evolving fintech landscape.

Funding Challenges: The UK’s Struggle to Support Startups

Fintech innovation in the UK is also significantly hindered by funding challenges, with entrepreneurs often struggling to secure necessary investment. Venture capital firms like Augmentum Fintech highlight that despite the UK’s robust startup ecosystem, many founders find it more fruitful to pursue their ventures in more lucrative markets such as those in Asia and the Middle East. A lack of accessible funding means that UK startups are not only hampered in their growth but are at risk of losing talent and innovation to countries willing to invest in their ideas.

Moreover, the downsides of Brexit continue to reverberate through the UK’s financial sectors, creating apprehension among investors impacted by the destabilization of international talent flow. Entrepreneurs must navigate not just regulatory pressures but also an increasingly competitive landscape where funding becomes harder to secure. If the UK wants to maintain its status as a financial hub, it needs to cultivate an environment more conducive to investment and innovation, ensuring that funds are readily available for new and promising fintech projects.

Emerging Fintech Hub: The Need for a Proactive Approach

Despite the current challenges, there remains potential for the UK to solidify its standing as an emerging fintech hub. To attract both domestic and international talent, UK regulators need to adopt a more balanced approach that embraces innovation while ensuring the safety of financial practices. The establishment of clearer guidelines for nascent technologies, especially within cryptocurrency and blockchain, could position the UK as an attractive destination for startups seeking certainty in a volatile marketplace.

Countries like Singapore and Hong Kong have shown how accelerated regulatory reforms can foster an environment where fintech enterprises can thrive. By taking cues from these examples, the UK can pivot to facilitate rather than hinder innovation, thereby ensuring a diverse and vibrant fintech community. The emphasis should be on collaboration between regulators and the fintech industry to create policies that not only protect consumers but also encourage entrepreneurial growth.

Cryptocurrency Challenges in the UK: Regulatory Impacts

The cryptocurrency sector in the UK is currently grappling with significant challenges, primarily stemming from an unclear regulatory framework. Industry leaders have voiced their frustrations regarding this lack of clarity, which prevents companies from launching innovative products such as stablecoins. Moreover, there is worrying discontent among crypto businesses about their banking relationships, with many reporting difficulties in opening accounts or sustaining existing ones due to their nature of operations. The regulatory landscape must evolve, addressing these barriers to enable a thriving crypto economy.

As the digital financial landscape evolves globally, the UK stands at a crossroads where it can either lead or lag behind in cryptocurrency adoption. Investors and entrepreneurs alike are keenly observing the regulatory decisions being made; the swift implementation of smart, supportive regulations akin to the EU’s MiCA could give the UK the competitive edge needed to retain its talent. Thus, proactive measures are paramount to ensuring that the UK can cultivate a robust cryptocurrency environment that appeals to innovators and investors.

The Importance of Clear Guidelines for Stablecoins

As blockchain technology continues to advance, the need for clear guidelines on stablecoins in the UK becomes increasingly critical. The success of potential stablecoin projects hinges on the ability to navigate regulatory complexities, which presently serves as a stumbling block for enterprises looking to launch such products. The UK must address these issues promptly to facilitate a smoother integration of stablecoins into the financial system, allowing firms to innovate without unnecessary constraints hindering their progress.

Industry insiders emphasize that a well-defined regulatory framework could not only ease the process for companies like ClearBank but also enhance public confidence in stablecoin adoption. With clear rules in place, the UK could strengthen its role as a leader in financial technology, reaping the benefits of a more comprehensive digital economy. The development of supportive measures, along with clear regulations, is vital for the growth and success of stablecoins and their rightful place in the financial services landscape.

The Global Fintech Race: Staying Competitive

As the global landscape for fintech continues to evolve, the UK must recognise the competitive race it is in against other international hubs. Countries like Singapore and Hong Kong have rapidly advanced their fintech sectors through regulatory reforms and clear guidelines, thereby attracting vast amounts of investment and talent. British leaders must take note and act quickly to ensure that the UK does not fall behind in this global race for fintech supremacy, which requires a commitment to innovation and regulatory evolution.

Competition means that in order to attract and retain fintech innovators, the UK must provide a supportive and enabling environment that nurtures growth rather than stifles it. Entrepreneurial spirit should be encouraged through less burdensome regulatory measures, allowing startups the freedom to flourish without the fear of excessive scrutiny or funding challenges. The time for action is now if the UK intends to maintain its esteemed position as a leading financial hub in the wake of rising competitors.

Brexit’s Ongoing Impact on the Fintech Sector

The ramifications of Brexit are ongoing and profound, especially for the UK fintech sector, which continues to feel the effects of reduced access to international talent and market fragmentation. As various companies have expressed concern over their capacity to attract the best minds in the industry due to tightened immigration rules, the competitiveness of the UK market is at stake. Restarting dialogues with the talent pool in Europe becomes crucial to sustaining innovation and ensuring UK startups have the capabilities needed to thrive.

As the UK faces these challenges, it’s essential for both government and industry leaders to collaborate and forge a unified vision that emphasizes the country’s advantages. With a talented workforce and a storied history of financial services, the UK can still emerge as a powerful player in the global fintech arena if it overcomes the obstacles posed by Brexit. Ensuring that the UK remains an attractive destination for professionals worldwide is imperative to bolstering its fintech capabilities.

The Role of Consumer Protection in Fintech Regulation

As the fintech and cryptocurrency spaces evolve, the balance between consumer protection and encouraging innovation becomes a critical discussion point for regulators. Striking this balance is essential; overly stringent regulations can result in innovation stagnation, while too lax an approach might expose consumers to significant risks. The role of regulatory bodies must therefore be seen as a facilitator of business development while ensuring that consumers remain safeguarded in a rapidly changing marketplace.

Creating a framework that recognises the necessity for innovation while prioritising user security will enhance consumer trust and engagement in the fintech space. Regulatory efforts should include transparent and clear communication with industry stakeholders to develop safeguards that support growth without compromising protection. By adopting such an approach, the UK can strengthen its regulatory framework, ensuring it encourages fintech innovation while still standing as a pillar of consumer protection.

Transitioning to a Supportive Ecosystem for Fintech

Transitioning to a more supportive ecosystem for fintech involves actively engaging with entrepreneurs to understand their needs and challenges. By fostering a culture of collaboration among regulators, established financial institutions, and startups, the UK can create an environment that enables innovation to thrive. This collaborative approach will not only benefit the emerging fintech companies but also enhance the competitiveness of the entire financial sector by promoting a diversity of services and solutions.

Such an ecosystem should include access to mentoring, networking opportunities, and funding initiatives geared toward startups. By embedding support mechanisms within the regulatory framework, the UK could lead the way in setting a precedent for how industry players and authorities can work together to build a robust, flexible fintech landscape. The successful transition to such an environment would ultimately retain and attract top talent and investment, ensuring the UK remains a fierce competitor in the global financial services theatre.

Frequently Asked Questions

What are the main cryptocurrency challenges facing the UK fintech sector?

The UK fintech sector faces several cryptocurrency challenges including overly stringent regulations, difficulties in securing bank accounts, and a lack of clear guidelines from the financial regulator. These issues discourage innovation and prompt cryptocurrency entrepreneurs to consider more favorable environments abroad.

How does the current regulatory landscape in the UK affect fintech innovation?

The current regulatory landscape in the UK is seen as restrictive, focusing too much on safety at the expense of innovation. This has led to a slowdown in the pace of fintech innovation, making the UK less competitive compared to other fintech hubs like Singapore and Hong Kong.

What impact does Brexit have on UK funding for startups in the fintech industry?

Brexit has created uncertainty in the UK, making it difficult for startup founders to secure funding. Many fintech entrepreneurs are increasingly looking to international markets such as the Gulf and US for capital, due to concerns over the local funding environment.

What steps is the UK taking to remain an emerging fintech hub?

To remain an emerging fintech hub, the UK must address both regulatory clarity and funding challenges. Recent proposals for regulating cryptocurrency firms aim to provide clearer guidelines, but industry leaders stress the need for swift action and supportive measures to attract and retain talent.

Why are emerging fintech companies considering moving out of the UK?

Emerging fintech companies are considering moving out of the UK due to the restrictive regulatory environment and difficulties in obtaining funding. Competing regions offer more favorable conditions for innovation, which can lead entrepreneurs to establish their ventures elsewhere.

How are UK regulators responding to the global fintech innovation trend?

UK regulators are beginning to acknowledge the need for more supportive measures as other regions, like the EU with its MiCA regulation, move swiftly to create clearer rules for cryptocurrency firms. However, the pace of these responses is seen as slow compared to competitors.

What are the implications of de-banking issues for cryptocurrency firms in the UK?

De-banking issues significantly impact cryptocurrency firms in the UK, as many struggle to obtain or maintain banking relationships. This lack of access to traditional financial services creates obstacles for growth and hinders the overall development of the UK fintech ecosystem.

What future challenges do UK fintech firms face regarding cryptocurrency regulations?

Future challenges for UK fintech firms include navigating complex regulations, particularly concerning stablecoins and ensuring compliance with evolving rules. Uncertainty in the regulatory framework may impede innovation and deter investment in the cryptocurrency sector.

| Key Points | Details |

|---|---|

| Regulatory Challenges | The U.K.’s financial regulator is seen as overly restrictive, hindering innovation in the fintech and cryptocurrency sectors. |

| Funding Issues | Entrepreneurs are struggling to secure funding within the U.K., prompting them to look abroad for opportunities. |

| Comparative Innovation | Other regions, particularly the U.S., Singapore, and Hong Kong, are perceived to be more innovative and friendly to fintech companies. |

| Impact of Brexit | Brexit has had enduring negative effects on the U.K. fintech sector, notably affecting the attraction of international talent. |

| Stablecoin Regulations | Draft proposals for regulating cryptocurrency in the U.K. are underway, but technical complexities remain a barrier. |

| Debanking Issues | Many crypto companies face challenges in opening and maintaining bank accounts in the U.K. |

| Industry Consensus | There is a collective call for clearer regulations to ensure the U.K. maintains its standing in global fintech. |

Summary

UK fintech regulation is imperative as the country faces a critical juncture in its digital finance landscape. Industry experts argue that without a more welcoming regulatory environment, the U.K. risks losing its competitive edge to emerging fintech and cryptocurrency hubs across the globe. To foster growth and maintain its position as a leader in this sector, the U.K. must adapt its approach to regulation, ensuring it balances innovation with safety to attract both talent and funding.