Avalanche price analysis reveals a notable bullish trend following a significant upward breakout recently observed in its daily chart. This surge allowed AVAX to exceed key technical indicators, including the 50 and 200 EMA, giving traders positive AVAX trading signals. As we delve deeper into the realms of crypto market trends, it becomes clear that the current price of Avalanche coin is poised for further movements, especially as it approaches the substantial resistance at the 800 EMA. The interplay of technical analysis AVAX suggests that if this resistance is breached, we could see a strong rally reflecting an AVAX bullish forecast. With the volume profile displaying a technical vacuum, traders should stay alert for sudden price impulses that could follow any breakthrough efforts in this pivotal zone.

Examining the price dynamics of Avalanche presents an intriguing perspective on the cryptocurrency’s trajectory in the market. The latest charts indicate a solid foundation for upward momentum, characterized by a robust bullish pattern. As analysts study the recent movements, attention is drawn to various resistance levels and support mechanisms that are shaping market behavior. In particular, the interplay of critical indicators is essential for understanding potential price actions for AVAX. As market participants look for signs of breakthrough opportunities, the implications of Avalanche’s recent performance reflect broader trends within the cryptocurrency sphere.

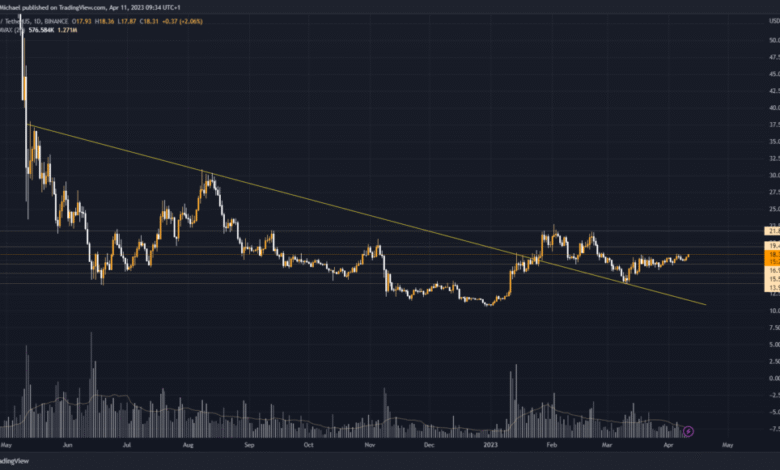

Avalanche Price Analysis: Technical Strength and Key Resistance Levels

Avalanche (AVAX) price analysis reveals a technically promising scenario on the daily chart. Recently, a classic W-formation breakout has been confirmed, signaling a potential bullish trend ahead. This upward movement allowed AVAX to surpass both the 50 EMA and the 200 EMA, crucial indicators in technical analysis that suggest growing strength in market sentiment. As AVAX approached the 800 EMA, it encountered a notable resistance area marking a critical point for traders to watch. Profit-taking actions at this juncture led to a temporary setback, yet the support from the 200 EMA has stabilized prices, indicating that the bulls are still contesting control of the market.

The breakout above key moving averages enhances the probability of a bullish forecast for Avalanche coin prices. With the current price hovering near significant horizontal resistance at the 800 EMA, traders should remain vigilant. The volume profile analysis sheds light on an area of historically low trading activity between the current price level and around $35, suggesting a technical vacuum. This lack of volume might lead to a swift price impulse if the resistance is decisively breached, highlighting the importance of maintaining awareness of crypto market trends while analyzing AVAX trading signals.

AVAX Trading Signals: Analyzing the Bullish Scenario on 4-Hour Chart

Analyzing AVAX trading signals on the 4-hour chart, we can identify a healthy correction phase that aligns with its overarching bullish trend. The pullback to the 800 EMA provides a significant opportunity for traders, given that this level has historically acted as a robust support zone. This confirms that market participants are increasingly interested in buying AVAX at these levels, as indicated by the notable recovery following the recent price adjustments. Surpassing the previous local high serves as a bullish indicator, suggesting that liquidity is being accumulated beneath the current price.

The current procyclical market structure indicates that buying dynamics dominate, provided there are no substantial selling pressures in the market. The technical indicators on the 4-hour chart emphasize the gradual buildup of long positions among traders, strengthening the case for a continued upward trend. In this context, well-informed trading strategies become essential for capitalizing on AVAX’s momentum and positioning effectively within the evolving crypto market landscape.

Understanding Technical Analysis for AVAX Traders

For traders looking to leverage Avalanche’s price movements, understanding technical analysis becomes crucial. The recent W-formation break on the daily chart is a classic signal many technical analysts seek for identifying potential trend reversals or continuations. Coupling this with indicators such as the 50 EMA and 200 EMA provides a clearer picture of market momentum. The geography of price, along with critical resistance areas, allows traders to devise strategies based on the volatility and price behavior of AVAX.

Integrating these technical insights with broader market trends will help refine trading approaches. For instance, AVAX’s movement towards the 800 EMA, supported by previous price action, underscores the importance of watching these levels closely. During periods of high volatility, traders can utilize caution while interpreting trading signals, particularly given the potential for sudden price actions in the crypto market. By mastering this technical framework, traders can better navigate the complexities of AVAX trading.

Exploring AVAX’s Support and Resistance Levels

Support and resistance levels are vital components of price action trading strategies for AVAX. The recent pullback to the 800 EMA on the 4-hour chart has reaffirmed this level as a dynamic support zone, suggesting that market participants are looking for buying opportunities at or near this point. As traders analyze these crucial levels, it becomes clear that a breach above the previous local high would strengthen the bullish sentiment, opening up further potential for price increases.

Additionally, traders should keep an eye on the horizontal resistance indicated at the 800 EMA; breaking through this level could initiate a significant price movement. Historically low trading volumes in this area present an opportunity for rapid price changes. Traders must remain prepared for swift actions and apply proper risk management techniques, especially as they analyze AVAX price movements in conjunction with broader market trends.

The Impact of Volume Profile Analysis on AVAX Trading

Volume profile analysis plays a critical role in understanding the price dynamics for Avalanche (AVAX). The recent observations indicate a low volume in the range between the current price and approximately $35, which heightens the chances for rapid price movements. Analyzing this volume profile data in conjunction with existing technical setups enables traders to identify potential breakouts or breakdowns effectively. Therefore, recognizing how volume interacts with price over time can be pivotal for successful trading.

This correlation between price and trading volume could lead to faster momentum shifts in the AVAX market. For informed traders, utilizing volume profile alongside traditional technical analysis tools offers a more rounded perspective. By keeping tabs on fluctuations in volume during price changes, traders can enhance their strategies and make educated decisions concerning entry and exit points.

Impact of Market Sentiment on Avalanche Price Trends

Market sentiment crucially influences price action, particularly in the volatile landscape of cryptocurrencies like Avalanche (AVAX). Sentiment can be gauged through various tools such as social media trends, trader sentiment surveys, or activity on trading platforms. In the case of AVAX, the recent uptick in bullish sentiment following the breakout of significant resistance exemplifies how traders react to technical indicators and macroeconomic factors alike.

Understanding market sentiment allows traders to better position themselves in the crypto market. When the sentiment aligns with technical analysis findings, such as the upward crossing of key moving averages, the likelihood of sustained price increases becomes significantly enhanced. Remaining updated on market news and technological advancements linked to Avalanche will further provide essential insights into potential future price actions.

Navigating the Current Avalanche Trading Environment

In the current trading environment, navigating Avalanche (AVAX) requires a nuanced understanding of technical analysis and market sentiment. With the recent breakout from the W-formation, traders are presented with fresh opportunities but also need to remain cautious. The interaction of the price with key EMAs indicates crucial decision-making points for both buyers and sellers in this market. Establishing clear trading plans that account for both upside potential and downside risks is necessary.

Furthermore, as the crypto landscape continues to evolve, it’s essential for traders to adapt their strategies accordingly. Observing changes in trading volumes, sentiment, and overall market trends can provide invaluable insights into the potential price direction of AVAX. By employing a balanced approach that integrates technical indicators and broader market analysis, traders can enhance their chances of success in the unpredictable world of cryptocurrency trading.

Crypto Market Trends Affecting Avalanche and AVAX

Current crypto market trends play a significant role in shaping the price momentum of Avalanche (AVAX). As the market continues to show signs of recovery and bullish patterns emerge, investor interest tends to spike, bringing higher liquidity and trading volumes. Such conditions create an environment conducive to price growth, allowing AVAX to capitalize on the positive market sentiment. Similarly, macroeconomic factors, including regulatory news or shifts in institutional investment perspectives, can dramatically influence price trends.

Traders must stay cognizant of these evolving trends and how they specifically relate to AVAX. By keeping track of upcoming events or developments within the broader crypto market, traders can better anticipate the effects on Avalanche’s price action. To remain competitive, incorporating insights garnered from ongoing market analysis will prove crucial for successful AVAX trading.

The Future of Avalanche: Analyzing Bullish Forecasts for AVAX

As we look to the future of Avalanche (AVAX), several bullish forecasts arise from current technical analysis and market conditions. The successful breaking of horizontal resistance levels, particularly at the 800 EMA, could signal further price increases in the long run. Analysts predict that if the positive momentum from recent bullish signals continues, AVAX could gain substantial ground, potentially reaching new all-time highs. This outlook aligns with the broader bullish sentiment currently seen in many market segments.

While forecasting positive price movements, it is essential to incorporate various factors such as market sentiment, external economic influences, and technological advancements related to the Avalanche blockchain. This comprehensive approach will empower traders and investors to maintain realistic expectations as they navigate potential price changes. Ultimately, a careful analysis paired with informed decision-making could lead to successful trading outcomes for AVAX in the months to come.

Frequently Asked Questions

What does Avalanche price analysis indicate about AVAX’s current market position?

Avalanche price analysis suggests that AVAX is currently in a strong position following a confirmed breakout from a classic W-formation. The price has surpassed important moving averages, indicating bullish momentum. As it approaches the 800 EMA, this level acts as resistance but has also shown potential as a dynamic support. This technical setup points towards an optimistic outlook for the Avalanche coin price, particularly if resistance is breached.

How do AVAX trading signals reflect the recent price movements of Avalanche?

Recent AVAX trading signals highlight a positive shift in market dynamics with the price bouncing off the 200 EMA, which now provides crucial support. The breakout past the previous local high underpins a bullish forecast for AVAX, suggesting further upside potential in the near term, especially if the price overcomes the 800 EMA resistance level.

What role does technical analysis play in Avalanche price analysis for AVAX?

Technical analysis plays a vital role in Avalanche price analysis by examining chart patterns, moving averages, and trading volume. The analysis indicates that after recent corrections, the price has found support at historical levels, such as the 800 EMA on the 4-hour chart. These technical indicators help traders make informed decisions based on market trends, enhancing the reliability of AVAX bullish forecasts.

What are the implications of the crypto market trends on Avalanche’s price forecast?

The current crypto market trends suggest a recovery phase for AVAX, supported by strong buying dynamics indicated through liquidity accumulation. As long as selling pressure remains minimal, these trends enhance the likelihood of a continued upward movement in Avalanche’s price. This aligns with a bullish outlook on the Avalanche coin price in the coming weeks.

Is a breakthrough of the 800 EMA critical for Avalanche’s future price movements?

Yes, a breakthrough of the 800 EMA is seen as critical for Avalanche’s future price movements. If AVAX can successfully breach this resistance, it may trigger a strong bullish impulse due to the low trading volume indicated by the volume profile. This could pave the way for a significant upward trend, reinforcing positive Avalanche price analysis.

| Key Point | Description |

|---|---|

| W-Formation Breakout | Avalanche recently broke upward from a classic W-formation, indicating strong bullish sentiment. |

| EMAs Dynamics | The price surpassed the 50 EMA and 200 EMA, showing strength in the medium-term market structure. |

| Resistance at 800 EMA | The price encountered resistance at the 800 EMA, leading to a temporary setback after hitting this horizontal resistance. |

| Dynamic Support | The 200 EMA is providing dynamic support, contributing to price stability after the recent breakout. |

| Volume Profile Insights | There is historically low trading volume between the current price level and $35, suggesting a potential for rapid price movement on breakout. |

| 4-Hour Correction Phase | A recent correction phase on the 4-hour chart reflects healthy market reactions, reaffirming the upward trend with the 800 EMA acting as support. |

| Market Dynamics | The buying dynamics currently dominate, with increased long positions and accumulation of liquidity, provided there are no significant selling reactions. |

Summary

Avalanche price analysis indicates a strong bullish outlook as the asset surpasses significant moving averages and shows resilience at key support levels. With the 800 EMA acting as a pivotal resistance point, traders should watch for a potential breakout that could lead to accelerated gains. A favorable volume profile further supports the likelihood of swift price movements, making AVAX a cryptocurrency to keep an eye on for both long-term and short-term trading strategies.